Can You Register a Hong Kong Company Remotely?

Yes, you can. A Hong Kong private limited company can generally be incorporated online, so you do not need to be physically in Hong Kong to complete the registration process.…

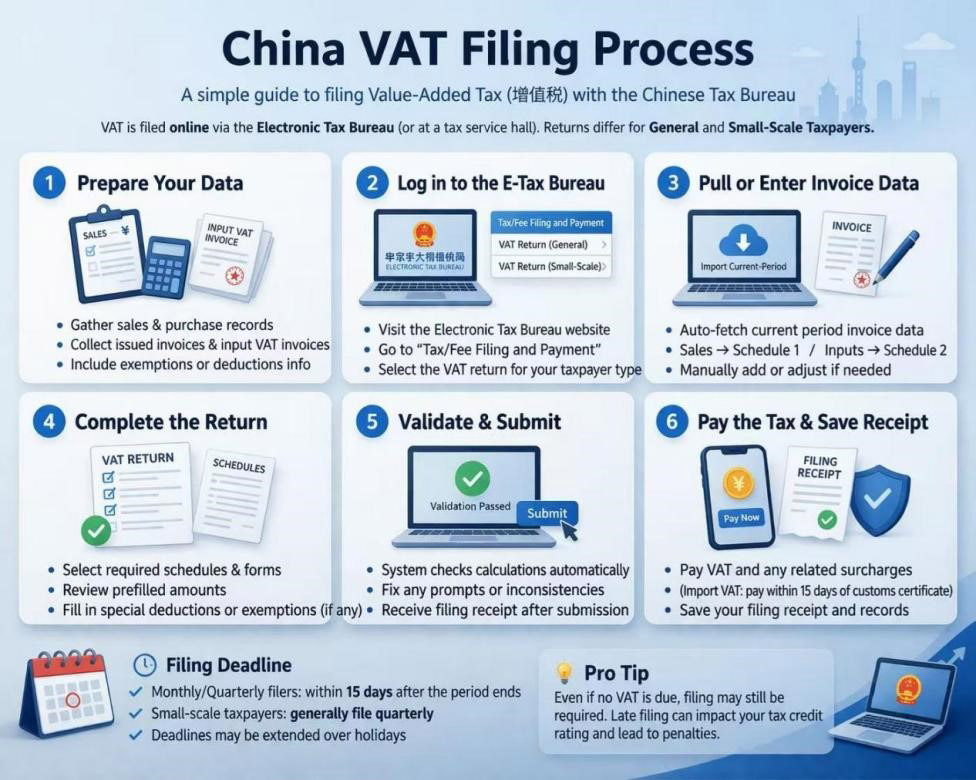

In China, VAT is typically filed with the tax bureau through the Electronic Tax Bureau, although filing at a tax service hall is also available. General taxpayers use the VAT and Surcharges Return for General Taxpayers plus the relevant schedules, while small-scale taxpayers use the small-scale taxpayer version of the return.

For timing, VAT filing periods can be monthly, or quarterly depending on the tax authority’s determination. In practice, monthly or quarterly filers must declare within 15 days after the end of the filing period. Official guidance also says small-scale taxpayers generally file quarterly, while certain general taxpayer categories may choose quarterly filing. Holiday calendars can extend a month’s deadline in specific cases.

A practical VAT filing workflow usually looks like this:

Gather sales records, purchase records, issued invoices, input VAT invoices, and any exemption or deduction information for the filing period. The official return instructions distinguish between goods, labor, and services/intangibles/real estate, and different schedules may apply depending on the transactions involved.

Go to Tax/Fee Filing and Payment, then select the VAT return for your taxpayer type. Official e-tax guidance shows this path for both general taxpayers and small-scale taxpayers.

The system can automatically collect current-period invoice data, and taxpayers can also manually adjust the return if needed. For general taxpayers, official guidance says sales invoice data can flow into Schedule 1 and input invoice data into Schedule 2, with automatic cross-form calculations and checks.

Select the required schedules, review the prefilled numbers, and complete any remaining business-specific fields, such as special deductions, simplified method items, or reduction/exemption details where applicable. Official instructions note that extra reduction/exemption schedules may be required when VAT incentives are claimed.

After the figures are checked, submit the return. The system runs validation checks, prompts you to correct inconsistencies if needed, and issues a filing receipt after successful submission. Official local guidance also notes that the system can then guide the taxpayer into the surtax filing step.

Once the return is accepted, pay any VAT and related surtaxes due, then save the filing receipt and archived return. For import VAT, payment is generally due within 15 days from the issuance of the customs import VAT payment certificate.

One useful reminder from official filing guidance: even where no VAT is payable for the period, filing obligations may still apply, and late filing can affect tax credit ratings and lead to legal consequences.

Hong Kong Tannet Group was founded in HK in 1999, now is in its sixth five-year development plan stage, and setting the upcoming two five-year plans. Over the past 28 years, HK Tannet Group has experienced significant growth and development, serves a diverse client base of over 100,000 customers from more than 130 countries. Tannet has been always devoted to providing with business solutions for investors all across the world. If you have any further inquiries, feel free to contact Shanghai Tannet at 0086-18101649652, email to tianyinong@tannet-group.com, or visit our website https://tannet-group.net/.